For banks, digital banks, and credit card companies, accurate transaction categorisation sits at the core of customer experience, analytics, compliance, and revenue optimisation. As consumers expect real-time insights and regulators demand clearer reporting, classification quality and proper transaction classification categories have become a competitive differentiator.

This article explains what financial transaction classification categories are, how they work, why they matter, and how institutions should design them for scale and accuracy.

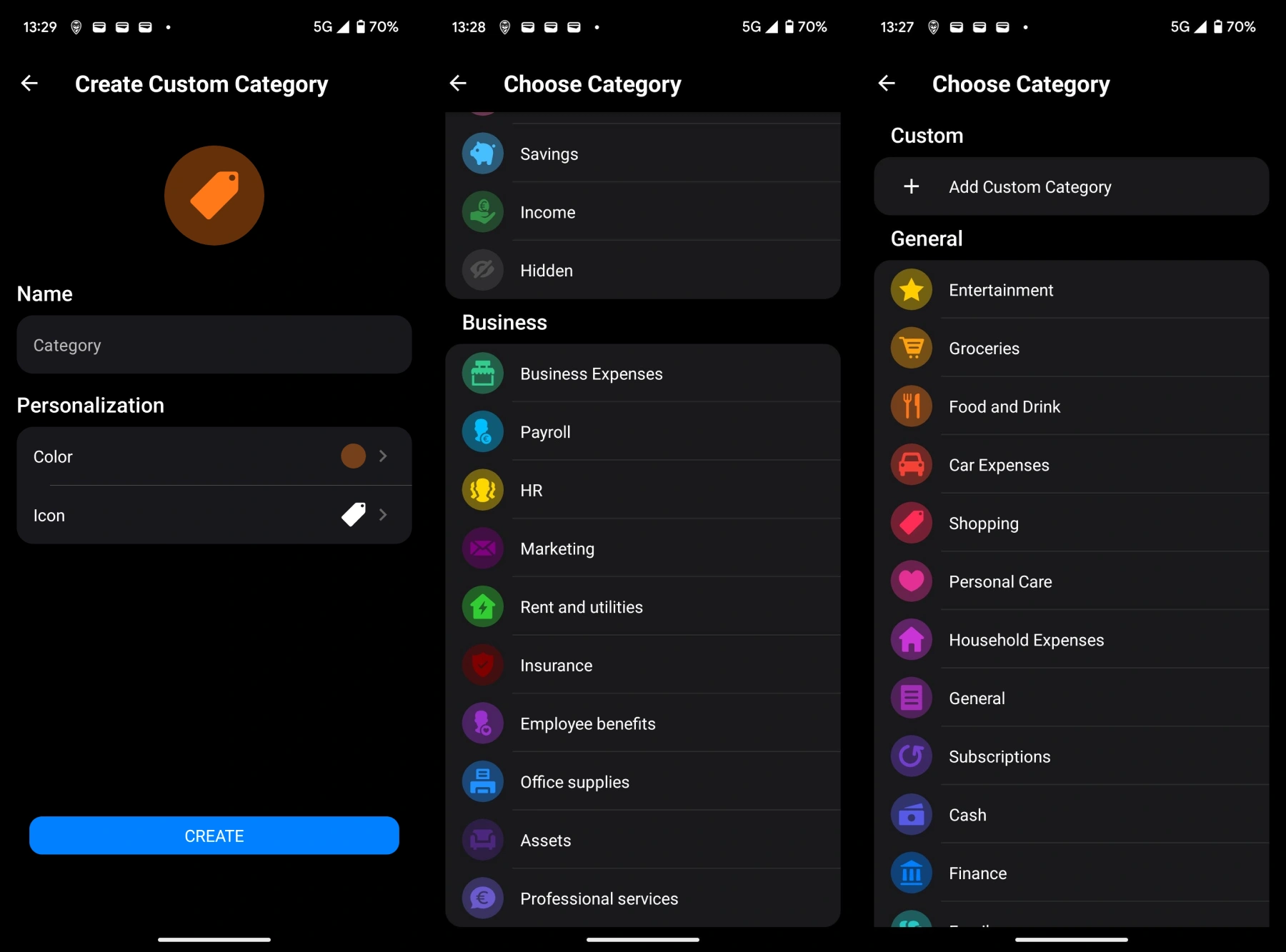

What are financial transaction classification categories?

Financial transaction classification categories are standardised labels applied to transactions to describe their economic purpose. Examples include income, groceries, dining, housing, utilities, transportation, subscriptions, transfers, fees, and investments.

For banks and card issuers, these categories upgrade and enrich raw transaction data with structured financial intelligence. They enable consistent reporting across channels, power customer-facing insights, and support internal analytics, risk monitoring, and regulatory obligations.

Well-designed categories strike a balance between clarity, consistency, and granularity, allowing institutions to understand spending behavior without overwhelming users or systems. It’s a win-win.

What is data quality? Learn more on our blog!

How transaction categorisation works in banking systems

Transaction categorisation relies on analysing multiple data points associated with each transaction, including merchant name, merchant category codes (MCCs), transaction description, amount, currency, location, frequency, and historical patterns.

Banks and digital banks typically use one or more of the following approaches:

- Rule-based logic, such as mapping MCCs to predefined categories

- Machine learning models trained on historical transaction data

- Hybrid systems combining deterministic rules with predictive models

Over time, these systems improve accuracy by learning from corrections, recurring transactions, and customer behavior. For credit card companies, this is particularly important given the volume, velocity, and diversity of card-present and card-not-present transactions.

Why is financial transaction classification important

Accurate transaction classification delivers value for banks and card issuers across multiple dimensions:

Customer Experience: Clear categories can properly support spending insights, budgeting tools, alerts, and rewards personalisation. Customers are more likely to engage with apps that clearly explain where their money goes.

Data Analytics and Optimalisation: Categorised data enables banks to analyse spending trends, identify cross-sell opportunities, optimise interchange strategies, and design targeted offers.

Risk, Fraud and Compliance: Structured transaction categories support anomaly detection, AML monitoring, dispute resolution, and regulatory reporting. Poor categorisation increases operational risk and manual review costs.

Operational Efficiency: Automated, high-confidence categorisation reduces the need for manual reconciliation, customer support interventions, and downstream data corrections.

Common financial transaction classification categories

Most banks and credit card companies use a consistent set of high-level categories, often aligned with industry standards and customer expectations:

- Income (salary, refunds, interest)

- Housing (rent, mortgage, property services)

- Food & Dining (groceries, restaurants, delivery)

- Transportation (fuel, public transit, ride-sharing)

- Utilities (electricity, water, internet, mobile)

- Entertainment & Lifestyle

- Subscriptions & Digital Services

- Shopping & Retail

- Healthcare

- Transfers & Payments

- Fees & Charges

- Savings & Investments

- Taxes & Government Payments

Subcategories are typically layered beneath these to support deeper insights while preserving usability, which is perfect for tools like PFM, credit scoring, or CO2 Insights. Â

How many transaction categories should banks use?

For most banking and card environments, best practice is to maintain 10-20 high-level categories, supported by 50-150 subcategories depending on product complexity and customer needs.

Too few categories limit insight and personalisation. Too many reduce classification accuracy, increase confusion, and degrade customer trust. Â

Want to know more? Read our deep dive into categorisation!

Best practices for digital and regular banks

There are several steps banks can take to maximise the value of financial transaction classification categories:

- Design categories around customer mental models that customers naturally understand: Groceries, Restaurants, Transport, Rent, Subscriptions, Shopping

- Continuously monitor accuracy and drift across merchants and regions. High-level categories should be boring, stable, and hard to break, while subcategories should carry the nuance.

- Allow controlled customisation without fragmentation. User edits are valuable, so allow them to reassign categories within the official taxonomy.

- Align categorisation strategy with fraud, rewards, and analytics teams. When teams use different category definitions, your bank runs four parallel versions of the same data.

- Treat categorisation as a core data product, not a one-time feature

Conclusion

For banks and credit card companies, financial transaction classification categories are foundational infrastructure. They build customer trust, unlock data-driven growth, and support regulatory resilience.

Institutions that invest in clear, scalable, and intelligent categorisation systems gain cleaner data and a strategic advantage in how customers understand and interact with their money.